The ISSB’s release of the IFRS S1 and IFRS S2

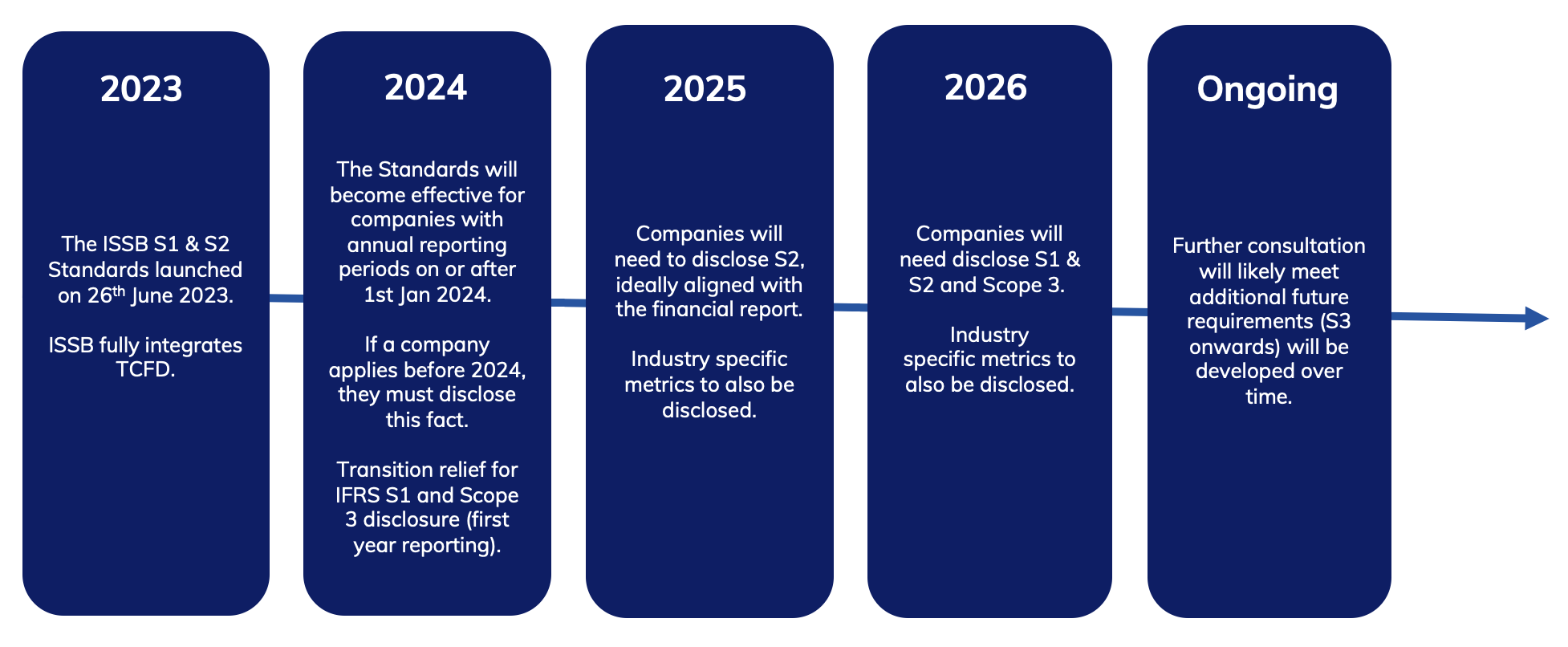

On 26th June 2023, the International Sustainability Standards Board (ISSB) published their inaugural global sustainability disclosure standards: The IFRS S1 and IFRS S2. This publication marks an important milestone as the standards aim to improve clarity in sustainability financial reporting by creating a “common language” for sustainability disclosure.

The IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information sets out the details for completing sustainability-related disclosures, whilst the IFRS S2 Climate-related Disclosures details the requirements for the measurement and disclosure of climate-related risks.

The ISSB has also fully incorporated the recommendations of the Task Force for Climate-related Financial Disclosures (TCFD) into the new standards.

What is the ISSB?

The ISSB was created in response to the increasing demand for clear and consistent sustainability reporting, as businesses face growing environmental regulations, climate-related risks, and investor expectations. The ISSB provides a trusted framework for financial markets to assess sustainability risks and opportunities, ensuring companies can transparently communicate their impact.

The ISSB aims to create a global baseline for sustainability information.

The ISSB was established to set a high-quality global standard for sustainability disclosures, giving investors and stakeholders reliable data to inform decision-making. Built upon the foundations of the IFRS accounting standards and the Sustainability Accounting Standards Board (SASB), the ISSB develops sustainability-related financial reporting that aligns with IFRS Sustainability Disclosure Standards.

“Over 20 jurisdictions representing nearly 55% of global GDP and 40% of global market capitalisation, have taken steps towards the introduction of ISSB standards into their regulatory frameworks”

ESG360°’s Key Takeaways:

TCFD Integrated:

As the TCFD has been fully integrated into the ISSB, the ISSB acts as the world’s first ever global ESG standard.

Further endorsement:

Backing of the International Organization of Securities Commissions (IOSCO) and the Financial Stability Board (FSB) is likely before the end of the year.

Assurance:

The ISSB is working in tandem with the International Auditing and Assurance Standards Board (IAASB) to create audit standards and internal controls for sustainability disclosures.

Industry Specific Metrics:

Industry specific metrics will be mandatory, in addition to scope 3 disclosure and scenario planning.

Climate-First Approach:

The ISSB prioritises a climate-first approach by focusing on climate-related disclosures through IFRS S2, ensuring companies assess and report climate risks before expanding to broader sustainability topics.

Climate Risk Quantification Project:

The International Accounting Standards Board (IASB) is embarking upon a climate risk quantification project, working with ISSB.

Comply-or-Explain:

The ISSB adopts a 'comply or explain' approach, allowing companies to either adhere to disclosure requirements or provide a clear justification for any omissions, ensuring flexibility while promoting transparency.

Transition Relief:

Companies will be allowed only to disclose IFRS S2 in the first year, as IFRS S1 and Scope 3 can be disclosed in the second year of adoption.

Transition Plan Disclosure:

The ISSB is encouraging companies to disclose their transition plan if they have one and the Transition Plan Taskforce (TPT) is aligning with the ISSB.

Sustainability Matters:

The consultation for other sustainability issues such as nature and biodiversity, just transition and human rights is open until September 2023.

IFRS S1 and S2 Timeline